I have to say that the World Cup sort of crept up on me and as a consequence I haven’t been able to work up the same enthusiasm as in the past. That is partly due to it appearing in the middle of the Premier League season, partly the playing conditions and partly the corruption associated with FIFA. After the FBI and Swiss authorities’ investigations into FIFA and the subsequent prosecutions it was hoped that the reputation of the worldwide football association would be restored. However, in the opinion of Mark Pieth, who was tasked to improve governance in the organisation, “the supposed modernization under current FIFA head Gianni Infantino has “plunged it into the Dark Ages of [former FIFA president Sepp] Blatter.” As Pieth notes, “they’re simply not up to regulating themselves.” Washinton Post 20/11/22. Which brings me to the reason for this essay. Not so much the question of corruption but the mention of the FIFA President, Gianni Infantino.

Gianni Infantino had taken on the responsibility of locating the 2022 World Cup to a venue that had no or, very little football infrastructure and a reputation for enforcing strict Sharia law. Knowing that this created issues for the ever-present alphabet soup community he received assurances that Sharia law enforcement would be relaxed for the period of the World Cup in Qatar. There was also the problem of migrant labour that was imported to build the football stadiums and associated facilities. Human Rights Watch, Amnesty and the Guardian, amongst others, have focussed on pay and conditions of these exploited workers. It is against this long-tailed background of complaints that my attention was drawn to the FIFA presidents inaugural address to open the competition. First of all, I must disclose that I didn’t listen to the full 57-minute speech. I don’t know anyone who did. Infantino started his speech in the manner of an inebriated father of the bride who, ignoring all the frozen stares of his family, made the occasion all about himself.

“Today I feel Qatari,” he said. “Today I feel Arabic. Today I feel African. Today I feel gay. Today I feel disabled. Today I feel [like] a migrant worker.” He added: “Of course I am not Qatari, I am not an Arab, I am not African, I am not gay, I am not disabled. But I feel like it, because I know what it means to be discriminated [against], to be bullied, as a foreigner in a foreign country. As a child I was bullied – because I had red hair and freckles, plus I was Italian, so imagine.” The Guardian, 19/11/22

Just a couple of points. Whilst not diminishing the effects of his early experience, hopping across the border from one western European country to another, bears no resemblance to the hardships suffered by foreign labourers working in Qatar. There is one ‘oppressed’ group that he missed, possibly because it is not recognised in the LGBTQ+ acronym, and that is, women. He hastily rectified this by adding this half of the population to the list of people he ‘feels like’ at least sparing us from describing women as ‘birthing people’. Was his empathy for everyone, other than white men, a criticism of his hosts anti gay laws, the hardship suffered by foreign workers and the restriction on women’s rights? From the excerpts of his speech that have surfaced, seemingly not. Like the drunken fathers speech, it is difficult to see what he did mean. By mentioning all the progressive shibboleths he must have known that this would highlight the cultural differences between the West and the hosts. In a further twist he had complained about some of the criticism he had received from Human Rights groups and he defended himself as follows

Infantino had suggested critics were “handing out moral lessons to the rest of the world” and said nations should “not allow football to be dragged into every ideological or political battle that exists”. The Guardian, 13/11/22

Does he not see the hypocrisy between his speech cataloguing all the groups driven by Western progressive ideology that he feels part of and his demand that Football be kept free of ideology and politics? To give him the benefit of the doubt I don’t think that he does. I think that he his so focussed on shameless and pathetic virtue signalling that it blinds him to the obvious contradictions in his position.

I could continue the drunken father analogy further but drinking in stadiums were suddenly forbidden two days before the start of the matches. However, that was not the only thing that seemed to break the peace negotiated with the Qatar authorities. Plans by European teams to display the LGBTQ+ rainbow colours came under attack and players who wore these emblems were threatened with punishment if they did not conform. Flags and emblems were also taken from supporters entering the stadium and FIFA seemed to be compliant with this. Gay rights campaigner Peter Tatchell said, “FIFA is now little more than a mouthpiece for the Qatari despots. It is giving cover for a sexist. Homophobic and racist dictatorship.’ Daily Mail 18/12/22. Infantino, who I believe expected applause from the progressives, was stung by the criticism and reacted with the racist card saying that Europeans should apologise for the past 3000 years history. Not withstanding the fact that there wasn’t a Europe at that time he defended the Qatar government and FIFA by charging opponents with Hypocrisy.

The view from Qatar was, you knew what you were getting into when you first took the money. You knew that we maintain a strict religious theocracy under Sharia law and you knew that we would defend our beliefs against Western decadence. They also, pointed out that, “Many here in Qatar are asking why there wasn’t a similar uproar when Russia hosted the World Cup in 2018 or when China hosted the Olympics in 2008; both countries with their own human rights issues.” (BBC News 23/11/22). It is a hard question to answer especially when you consider the questionable FIFA bidding process. There was another group of less than heroic’ standing, defending the rights of the alphabet soup community, who caved in to the pressure from the Qatar Government. As reported by Forbes, “The national soccer federations of the Netherlands, England, Wales, Belgium, Switzerland, Germany and Denmark issued a joint statement announcing they are backing off, stating they did not want to put their players “ in a position where they could face sporting sanctions.” (Forbes 21/11/22) Meanwhile the families of the Iranian Team were reportedly under threat because the team didn’t sing the national anthem in protest against the death of Mahsa Amini. The lesson to take away from this is that it is easy to ‘take the knee’ in a Western country where there is no consequence for doing so, than in countries like Qatar and Iran.

What do we take from the speech and events surrounding the World Cup. First of all, the very bad news is that Infantino is making a bid to remain as FIFA President until 2031. That means a constant flow of corruption, contradictory policies and meaningless self congratulatory virtue signalling. Secondly, this will be matched by sporting administrators and over paid sports men and women. (Assuming we still recognise biological men and women in 2031). Infantino is your quintessential example of someone who see’s a role beyond that in the job description. He see’s himself as a major political force and is prepared to compromise his responsibilities to football to further his ambition. This is a modern trend and is borne out of lack of a sense of duty toward those for whom you are responsible and a lack of humility. Three thousand years ago, Infantino would know that the Greeks had a god named Hubris who represented arrogance, lack of humility, wanton violence etc. What he seems to have forgotten is that this god is followed by another called Nemesis, the goddess of fate and retribution. Perhaps, the goddess Nemesis would save us from an extended term of President Infantino and allow him to be replaced by someone who has the best interests of the game at heart instead of the corruption, arrogance and virtue signalling of Gianni Infantino.

Sources

Dan Hough, 20/11/22, The Washington Post, Qatar is taking the heat for FIFA corruption, washingtonpost.com/politics/2022/11/20/fifa-qatar-world-cup-corruption/

Sean Ingle, 19/11/22, The Guardian, ‘I feel gay, disabled … like a woman too!’: Infantino makes bizarre attack on critics, theguardian.com/football/2022/nov/19/fifa-gianni-infantino-world-cup-qatar

Shanti Das, 13/11/22, The Guardian, Anger over Fifa president’s ‘stick to football’ letter to World Cup teams, theguardian.com/football/2022/nov/13/anger-over-fifa-presidents-stick-to-football-letter-to-world-cup-teams

Shaimaa Khalil, 23/11/22, BBC News, World Cup 2022 armband row: ‘Two parallel universes on human rights controversies’, bbc.co.uk/sport/football/63718164

Siladitya Ray, 21/11/22, Forbes Business, World Cup: Teams Will Not Wear Rainbow Armbands After FIFA Threatens Yellow Cards, www.forbes.com/sites/siladityaray/2022/11/21/world-cup-teams-will-not-wear-rainbow-armbands-after-fifa-threatens-yellow-cards/?sh=511d320e4bd3

“This image shows the gestational sac of a nine-week pregnancy. This is everything that would be removed during an abortion and includes the nascent embryo, which is not easily discernible to the naked eye.” Dr. Joan Fleischman

“This image shows the gestational sac of a nine-week pregnancy. This is everything that would be removed during an abortion and includes the nascent embryo, which is not easily discernible to the naked eye.” Dr. Joan Fleischman The thing that struck me about the subtitle and large parts of the MYA supplied data was the constant reference to ’tissue’ when we would normally be talking about the embryo or, the foetus. To be fair there is a reference to the aborted embryo in the above picture but it, ” … is not easily discernible to the naked eye” I don’t understand why that means it can’t be shown in the photograph by enlarging it to scale. This is important because the thrust of the article is to depersonalise and dehumanise the foetus. What we are shown is not, “everything that would be removed during an abortion” but some innocuous cotton wool like material that has no potential for life. There is no attempt to argue against the above chart which shows the development of a child but by using the artifice of showing only, the tissue, seeks to persuade people that there is no moral or, criminal argument to be made against them.

The thing that struck me about the subtitle and large parts of the MYA supplied data was the constant reference to ’tissue’ when we would normally be talking about the embryo or, the foetus. To be fair there is a reference to the aborted embryo in the above picture but it, ” … is not easily discernible to the naked eye” I don’t understand why that means it can’t be shown in the photograph by enlarging it to scale. This is important because the thrust of the article is to depersonalise and dehumanise the foetus. What we are shown is not, “everything that would be removed during an abortion” but some innocuous cotton wool like material that has no potential for life. There is no attempt to argue against the above chart which shows the development of a child but by using the artifice of showing only, the tissue, seeks to persuade people that there is no moral or, criminal argument to be made against them.

I had been following the case of the January 6th rioters/protesters in the US who had been arrested but held on remand for, in some cases, over seven months in conditions that would not be accepted for convicted criminals. In this case the presumption of innocence seems to have been suspended for purely political reasons. It was with these thoughts in mind that I saw that a conviction for rape had been quashed in the High Court, in the UK, after the discovery of new evidence that was not put before the Jury at the original Trial in 2013. The reason for my interest was that the issue of consent was at the centre of the prosecution’s case which meant that the Jury had to make it’s decision on whose evidence it found more believable. The accuser presented an edited number of posts which supported her claim that there was little contact between her and the accused after sex. The accused, Danny Kay, asked the prosecution to assist in recovering the deleted messages but this wasn’t done and he was sentenced to four and a half years in prison. It was his sister-in-law who discovered the backup files which were the basis for his successful appeal. The Appeal Judge, Mr Justice James Goss said: “We have come to the conclusion that, in a case of one word against another, the full Facebook message exchange provides very cogent evidence both in relation to the truthfulness and reliability of (the woman) … and the reliability of (Mr Kay’s) account and his truthfulness.” (BBC 22/12/20) Mr Kay was released from prison after serving two years of his sentence. Before we get to the question of presumption of innocence I would like to comment on the police and prosecution’s lack of competence in this case. Mr Kay had warned them that the evidence on which they based their case was misleading and edited but with all the technical expertise at their disposal it was the defendants sister-in-law who found the evidence that was so compelling to the Court of Appeal. Mr Kay’s lawyer said, “Danny’s case is slightly unusual because all reasonable lines of inquiry don’t necessarily seem to have been followed,” (BBC 5/1/18). You don’t say!

I had been following the case of the January 6th rioters/protesters in the US who had been arrested but held on remand for, in some cases, over seven months in conditions that would not be accepted for convicted criminals. In this case the presumption of innocence seems to have been suspended for purely political reasons. It was with these thoughts in mind that I saw that a conviction for rape had been quashed in the High Court, in the UK, after the discovery of new evidence that was not put before the Jury at the original Trial in 2013. The reason for my interest was that the issue of consent was at the centre of the prosecution’s case which meant that the Jury had to make it’s decision on whose evidence it found more believable. The accuser presented an edited number of posts which supported her claim that there was little contact between her and the accused after sex. The accused, Danny Kay, asked the prosecution to assist in recovering the deleted messages but this wasn’t done and he was sentenced to four and a half years in prison. It was his sister-in-law who discovered the backup files which were the basis for his successful appeal. The Appeal Judge, Mr Justice James Goss said: “We have come to the conclusion that, in a case of one word against another, the full Facebook message exchange provides very cogent evidence both in relation to the truthfulness and reliability of (the woman) … and the reliability of (Mr Kay’s) account and his truthfulness.” (BBC 22/12/20) Mr Kay was released from prison after serving two years of his sentence. Before we get to the question of presumption of innocence I would like to comment on the police and prosecution’s lack of competence in this case. Mr Kay had warned them that the evidence on which they based their case was misleading and edited but with all the technical expertise at their disposal it was the defendants sister-in-law who found the evidence that was so compelling to the Court of Appeal. Mr Kay’s lawyer said, “Danny’s case is slightly unusual because all reasonable lines of inquiry don’t necessarily seem to have been followed,” (BBC 5/1/18). You don’t say! A recent decision by the Court of Appeal caught my eye because it concerned housing self identified female trans prisoners in female prisons. My interest had been tweaked because I had referenced a similar case in an essay in April 2019. (

A recent decision by the Court of Appeal caught my eye because it concerned housing self identified female trans prisoners in female prisons. My interest had been tweaked because I had referenced a similar case in an essay in April 2019. (

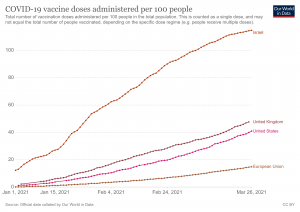

The real problem is there for everyone to see and is shown in the following graph. The one on the left shows the number of vaccinations administered per 100 for Israel, the US, the UK and the EU . Israel leads the group with the US and UK following at a much lower rate with the EU trailing far behind. There were many problems for the EU in trying to co ordinate an effective vaccination program with 27 countries. These include, inter alia, a slow bureaucracy, national antipathy, lack of confidence in vaccines, lack of confidence in the Commission and energy expended refighting the last war. If we take one element, that of the time taken to approve the Oxford Astra Zeneca vaccine we can see delay after delay whilst the UK fast tracked the process. At the same time the vaccine was being tested, a huge campaign was launched by the NHS to ensure the public had confidence in the product. Oddly enough, you could take the words from a critic of Astra Zeneca and apply it to the EU roll out. Just imagine ‘EU’ in place of ‘Astra Zeneca’ as the subject in the following extract from a BBC interview with Mr Lamberts MEP, in which he states “They commit, they de-commit, they de-commit on new commitments without any warning.” Of course he was talking about the rollout issues and Astra Veneca’s difficulty in resolving them but the quote sums up the companies problems dealing with the EU. In short, the European Medicines Agency (EMA) approved the Oxford Astra Zeneca vaccine, after some delay, in January. Some EU countries were not happy with the statistics for the older age groups and restricted it’s use for the over 65’s. By March, France and Germany approved it for the 65 -74 age group but delayed again over fear of people developing blood clots post vaccination. EMA reassured them that there was no evidence to support these fears and distribution restarted with France restricting use to the over 55’s. Now, Germany has again stopped vaccination despite assurances from the EMA and the Commission. The absence of trust in the EU institutions and seemingly non scientific bias locally has created mistrust in the vaccine as seen in the graph from the Economist, below.

The real problem is there for everyone to see and is shown in the following graph. The one on the left shows the number of vaccinations administered per 100 for Israel, the US, the UK and the EU . Israel leads the group with the US and UK following at a much lower rate with the EU trailing far behind. There were many problems for the EU in trying to co ordinate an effective vaccination program with 27 countries. These include, inter alia, a slow bureaucracy, national antipathy, lack of confidence in vaccines, lack of confidence in the Commission and energy expended refighting the last war. If we take one element, that of the time taken to approve the Oxford Astra Zeneca vaccine we can see delay after delay whilst the UK fast tracked the process. At the same time the vaccine was being tested, a huge campaign was launched by the NHS to ensure the public had confidence in the product. Oddly enough, you could take the words from a critic of Astra Zeneca and apply it to the EU roll out. Just imagine ‘EU’ in place of ‘Astra Zeneca’ as the subject in the following extract from a BBC interview with Mr Lamberts MEP, in which he states “They commit, they de-commit, they de-commit on new commitments without any warning.” Of course he was talking about the rollout issues and Astra Veneca’s difficulty in resolving them but the quote sums up the companies problems dealing with the EU. In short, the European Medicines Agency (EMA) approved the Oxford Astra Zeneca vaccine, after some delay, in January. Some EU countries were not happy with the statistics for the older age groups and restricted it’s use for the over 65’s. By March, France and Germany approved it for the 65 -74 age group but delayed again over fear of people developing blood clots post vaccination. EMA reassured them that there was no evidence to support these fears and distribution restarted with France restricting use to the over 55’s. Now, Germany has again stopped vaccination despite assurances from the EMA and the Commission. The absence of trust in the EU institutions and seemingly non scientific bias locally has created mistrust in the vaccine as seen in the graph from the Economist, below.